How To Win Against Velocity Investments: Beat Debt Collectors

If Velocity Investments contacts you, validate the debt first before paying anything. You can negotiate settlements for 40-60% of the original balance by making written offers and requesting payment plans. If sued, you must respond to the lawsuit by the deadline to avoid automatic judgment and wage garnishment.

Answer Your LawsuitVelocity Investments may be contacting you about an unpaid debt. You got behind on payments for a credit card, medical bill, or loan. Now Velocity wants their money. They’re a debt collection company that works for original creditors and debt buyers. Sometimes they purchase debts themselves.

You have options. You can fight back. Here’s how to win against Velocity Investments.

Being Sued by Velocity Investments? Respond in 15 Minutes

Don't let Velocity win by default. Our partner Solo has helped over 300,000 people answer debt lawsuits and negotiate settlements. Get started now with a 100% money-back guarantee.

Respond to Lawsuit NowDo You Have To Pay Velocity Investments?

Hold on. Don’t pay anything yet. First, make sure they validate the debt and its details. Confirm the debt is actually yours. Check that the amount is correct. Verify that Velocity owns the debt.

If everything checks out, you probably need to pay something. But you don’t have to pay the full amount.

Ignoring Velocity leads to serious consequences. Your credit score will tank. Your wages could be garnished. Your bank account could be frozen. Responding is always better than hiding.

Here’s the good news: debt collectors expect negotiation. Many people settle for 40-60% of the original debt. You can get rid of financial burden and emotional stress.

Negotiate a Settlement With Velocity in 3 Steps

Debt collection is lucrative for companies like Velocity. Surprisingly, that works in your favor.

When Velocity collects for original creditors, they earn a percentage. When they buy your debt, they paid pennies on the dollar. Either way, they profit even without collecting the full amount.

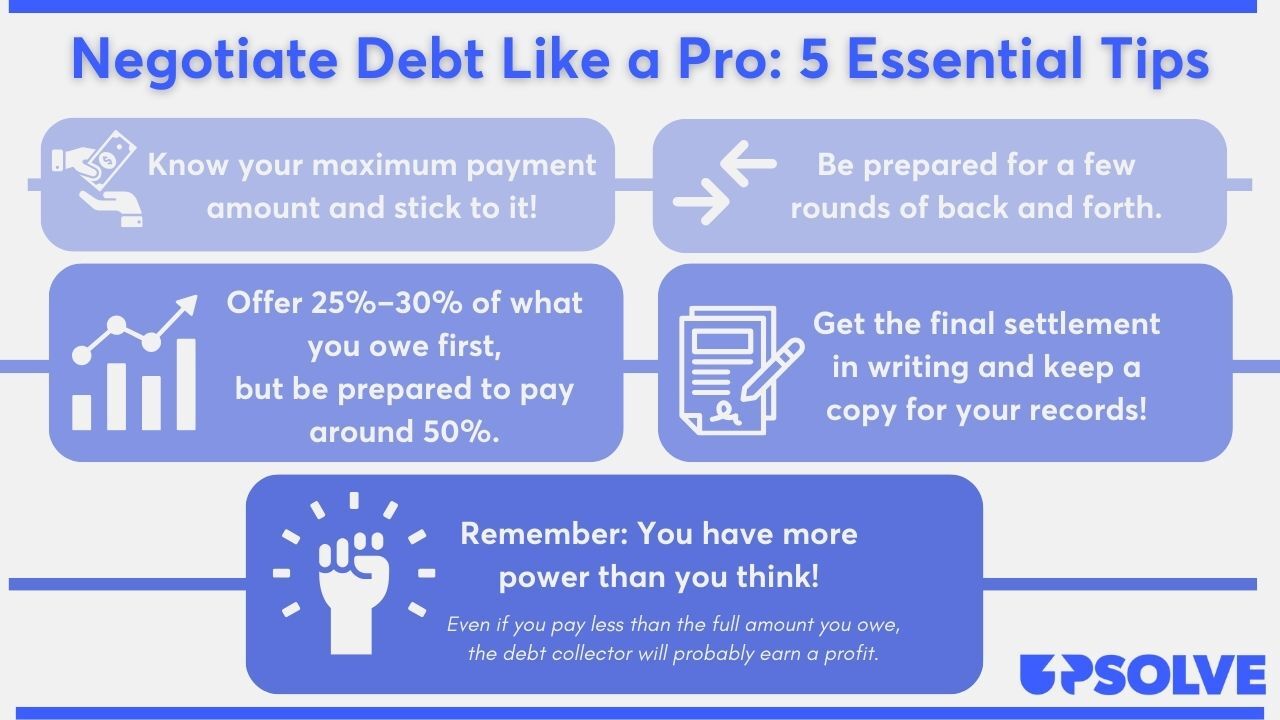

Start by offering 25% of what you owe. Expect a counteroffer. Most collectors settle between 40-60% of the original balance.

You can start the conversation. Don’t wait for them to reach out first.

Step 1: Validate the Debt

Validation comes first. Always. You need to confirm three things:

- The debt belongs to you (no identity theft or mistaken identity)

- Velocity owns the debt or has legal rights to collect

- The amount is accurate

Velocity must send you a debt validation letter. Federal law requires this within five days of initial contact. The letter should include all debt details.

Haven’t received it? Ask for one immediately.

Need more information? Send Velocity a debt verification letter. You have 30 days to dispute the debt. Velocity cannot take action during this window.

Step 2: Calculate What You Can Pay

Velocity validated the debt. You agree you owe it. Now figure out what you can afford.

Don’t sacrifice essentials like food or housing. Look at your monthly take-home pay. List your expenses. Account for other debt payments.

Consider getting free help from a nonprofit credit counselor. Financial professionals can review your debt-relief options. Our partner Cambridge Credit Counseling offers free consultations.

Choose Your Payment Method

You can pay in two ways: lump sum or payment plan.

Debt collectors prefer lump-sum payments. Less risk of non-payment. Consider using a tax return or work bonus. Make it count.

Can’t do lump sum? Negotiate a payment plan instead. Offer direct bank withdrawal to sweeten the deal. Make sure you can afford what you promise.

Step 3: Make Your Settlement Offer

You’ve done the math. You know what you can pay. Time to make your offer.

Put everything in writing. You need a paper trail. Use a debt settlement letter template to draft your proposal. Request Velocity’s reply in writing too.

Negotiate Everything, Not Just the Amount

Don’t stop at the settlement amount. Negotiate how you’ll repay. Negotiate credit report language too.

Velocity can report your account three ways: paid in full, partial payment, or settled. Ask them to report it as paid in full. Your credit score will thank you later.

Can You Settle After Being Sued?

Yes. You can usually negotiate even after a lawsuit starts.

But you must respond to the lawsuit. Attend court hearings. Reply to court notices. Keep negotiating, but treat the case as real.

Ignore the court and you’ll lose. Velocity gets a judgment. Then comes wage garnishment. Or bank account levies.

The case stays valid until the judge dismisses it. Need help responding? Our partner Solo specializes in debt lawsuit defense.

Settlement Success Tips

Negotiating feels scary. But it’s easier than you think. Here’s how to succeed:

- Always get agreements in writing

- Never share bank account information until you have a signed agreement

- Start with a low offer (25-30% of the debt)

- Stay calm and professional during negotiations

- Don’t make payments you can’t afford

- Request debt deletion from your credit report

- Keep copies of all correspondence

For more strategies, read our article on negotiating with debt collectors.

How To Beat Velocity in Court

Velocity probably won’t sue you first. But they might if collection attempts fail repeatedly.

You’ll receive a summons and complaint. These are official court documents. The summons tells you about the lawsuit. The complaint lists the claims against you.

Responding is critical. You can do it yourself. No lawyer required.

Ignore the lawsuit and Velocity wins automatically. They get a court order. Your wages get garnished. Your bank account gets frozen.

Our partner Solo has helped over 300,000 people respond to debt lawsuits. They offer a 100% money-back guarantee.

Step 1: Read Your Court Documents

The summons includes key information you need:

- Court name and address

- Names and contact information of both parties

- Case number

- Nature of the lawsuit

- Consequences of not responding

- Response deadline

Circle the response deadline. Mark your calendar. Miss this date and you lose.

The complaint lists claims against you in numbered paragraphs. Read each one carefully.

Step 2: Complete Your Answer Form

Your answer form is your defense. You explain why Velocity shouldn’t win.

Many courts provide answer forms. Sometimes they come with the summons. Other times you’ll find them on the court website. Search for the court name plus “answer form.”

Read the instructions carefully. Follow each step exactly. Some courts require additional forms like a certificate of service.

Each court has different rules. The court clerk can help you understand processes and paperwork. They can’t give legal advice, but they guide you through procedures.

Confused about your defense? Our partner Solo can help you draft a winning answer to your summons.

Step 3: File and Serve Your Answer

Filing options vary by court. You can usually file in person at the courthouse. Certified mail works too. Some courts accept email or e-filing.

Check your summons for filing instructions. Or contact the court clerk.

You also need to serve Velocity. Send them a copy of your answer. Mail it to the address on the summons. Use certified mail with return receipt.

Your Next Steps

Velocity Investments contacted you about a debt. Validate it first. Dispute invalid debts immediately.

Valid debt? Time to negotiate. Calculate what you can afford. Make an offer in writing. Aim for 40-60% of the original balance.

Got sued? Respond to the lawsuit before the deadline. Our partner Solo can help you answer the summons and negotiate a settlement.

Check your court’s website for specific processes. Contact the court clerk with questions. You have more power than you think.