How to Make a Debt Validation Letter That Works (2025 Guide)

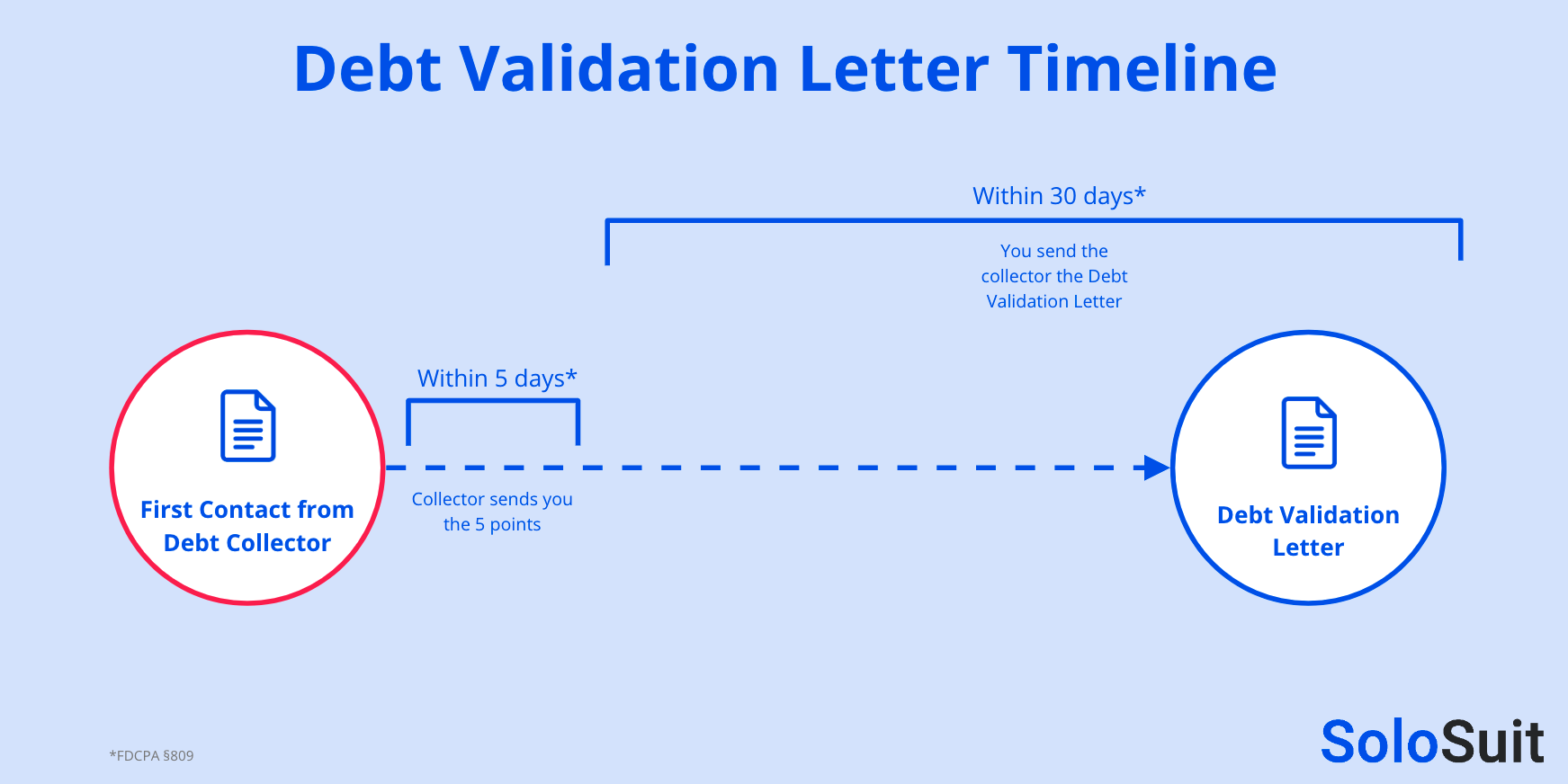

A debt validation letter is your strongest tool against debt collectors. Send it within 30 days of first contact to force collectors to prove you owe the debt. If they can't validate it, they must stop collection efforts and remove negative marks from your credit report.

Respond to CollectorsU.S. household debt hit $17.29 trillion in 2024. Credit cards, mortgages, and auto loans keep climbing.

Many consumers discover they don’t actually owe the debts collectors claim. You have the right to challenge these claims.

Stop Collectors From Harassing You Today

Don't let debt collectors bully you into paying debts you don't owe. Get expert help to respond to collection attempts and negotiate settlements within 30 days.

Answer Your LawsuitA debt validation letter protects you from bogus collection attempts. You’ll learn how to create one and why it works.

What Is a Debt Validation Letter?

A debt validation letter is your written request for proof. You send it to a debt collector asking them to verify the debt is real and belongs to you.

You have 30 days from initial contact to send this letter. Don’t waste that window.

Your Legal Right to Request Validation

The Fair Debt Collection Practices Act gives you protection. Collectors must follow specific rules.

Within five days of contacting you, collectors must provide:

- The amount you allegedly owe

- The creditor’s name

- Notice that you can dispute within 30 days

- Agreement to send validation if you request it

- The original creditor’s name and address upon request

You then have 30 days to dispute the debt. Section 809(b) of the FDCPA states collectors must stop collection until they validate the debt.

If collectors violate these rules, you can sue for $1,000 or more. Missing the 30-day deadline weakens your position but doesn’t eliminate your rights.

Three Steps to Make Your Debt Validation Letter

Creating an effective letter takes just three simple steps. You’ll protect your rights and force collectors to prove their claims.

Step 1: Assert Your Rights

Start by citing the FDCPA. Collectors need to know you understand your rights.

Include these specific demands:

- Contact me only to validate the debt

- Report to credit bureaus that I dispute this debt

- Stop all contact except to notify me of legal action

Threaten legal action for FDCPA violations. Collectors take these threats seriously.

Step 2: Request Validation

Make collectors prove every aspect of the debt. Ask for:

- Proof you owe this specific debt

- The exact amount owed

- The age of the debt

- Documentation showing they own the debt

- Their license to collect in your state

- Statute of limitations calculation

- The last payment you made on this account

These requests form the core of your letter. The more specific you are, the harder it becomes for collectors to respond.

Need help getting started? Our partner Solo provides templates and guidance for debt validation letters.

Step 3: Send the Letter

Print your letter and use trackable mail. USPS Priority Mail costs $7.50 and provides tracking.

Skip certified mail with return receipt. Priority Mail arrives faster and costs less.

Mail the letter to whoever contacted you most recently. That could be an attorney or collection agency.

How Debt Validation Letters Stop Collection Calls

Banks sell unpaid debts for about 4% of their value. Debt collectors buy these debts in bulk.

Documentation is often incomplete. Collectors may struggle to prove ownership or verify who owes what.

Your validation letter raises their costs. That makes collection less profitable and more likely they’ll drop the case.

The letter stops calls in two ways:

- Under FDCPA Section 809(b), collectors must cease communication when you dispute the debt

- Under FDCPA Section 805(c), you can demand they stop contacting you entirely

If they keep calling after receiving your letter, they’ve violated federal law.

Free Debt Validation Letter Template

Use this template to assert your rights. Customize it with your specific information.

[Your Name]

[Your Address]

[City, State, ZIP Code]

[Date]

[Debt Collector’s Name]

[Debt Collector’s Address]

[City, State, ZIP Code]

Re: [Account Reference Number]

Dear [Debt Collector’s Name],

I am writing in response to your [letter/call] dated [date] regarding an alleged debt. Under the Fair Debt Collection Practices Act, Section 809(b), I request validation of this debt.

Please provide the following information:

- The amount of the debt

- The name of the original creditor

- Documentation proving I have a legal obligation to pay

- Verification that the debt is within the statute of limitations

Until this debt is validated, all collection activities must cease. I am not acknowledging this debt, but exercising my rights to dispute it.

I expect your response within the legally mandated timeframe.

Sincerely,

[Your Name]

Should You Always Send a Debt Validation Letter?

Yes, almost always. The letter forces collectors to take you seriously.

49% of FTC complaints about debt collectors involve debts consumers don’t owe. 53% of people contacted by collectors say the debt is wrong or not theirs.

You’re not alone if you’re being hounded for money you don’t owe.

Failing to dispute gives collectors permission to assume the debt is valid. You’re surrendering your rights by staying silent.

Why Debt Validation Letters Work

Here’s why these letters benefit you in nearly every situation:

- If you don’t owe the debt, collectors likely can’t validate it

- If you owe only part of the debt, collectors must prove the exact amount

- Even if you owe the full amount, collectors may lack proper documentation

- Collectors might not be able to prove they own the debt

- You gain information to negotiate a better settlement

Every scenario works in your favor when you request validation.

Dealing with aggressive collectors? Our partner Solo helps you respond to debt collection lawsuits and negotiate settlements.

What Happens If Collectors Don’t Validate the Debt?

They’ve violated the FDCPA. You can sue for $1,000 per violation.

Report them to your state attorney general, the FTC, and the Consumer Financial Protection Bureau.

Without validation, they cannot continue collection efforts. They cannot sue you. They must remove negative marks from your credit report.

What If Collectors Successfully Validate the Debt?

You still have options even if they provide proper documentation:

- Send a cease and desist letter to stop all contact

- Offer to settle for a percentage of the debt

- Wait for the statute of limitations to expire

- Negotiate a payment plan

Settling for less than the full amount is often your best move. Many collectors accept 25-50% of the original debt.

Using Debt Validation Letters for Medical Bills

Medical debt works the same way. Validation letters are powerful for healthcare collections.

Medical billing errors are common. You might receive bills for balances you already paid or services you never received.

Scammers also send fake medical bills in mass mailings. A validation letter stops these fraudsters immediately.

Medical providers must prove the debt before reporting it to credit bureaus or filing lawsuits.

What to Do After Mailing Your Letter

Follow these two critical steps:

- Check your credit report to confirm the debt appears as disputed

- Keep detailed records of all correspondence with collectors

Take photos of every letter and document. If you didn’t document it, it didn’t happen.

What If You Missed the 30-Day Deadline?

You can still send the letter. It just won’t carry as much legal weight.

The FDCPA doesn’t explicitly state what happens after 30 days. Your letter can still have an impact.

Failing to dispute doesn’t equal admission of guilt. You can still win a future lawsuit even without sending the letter.

But don’t take chances. Send the letter as soon as you learn about the debt.

Can Collectors Contact You After Validation Requests?

Collectors can only contact you to:

- Notify you they’re ending collection efforts

- Inform you they have the right to sue you

- Tell you they plan to file a lawsuit

FDCPA Section 805(c) prohibits all other contact. If they call for any other reason, they’ve broken federal law.

Keep records of any violations. Each one could be worth $1,000 in a lawsuit.

What If a Collection Agency Never Contacted You?

Debts can appear on your credit report without warning. You might be sued without prior contact.

If you’re sued, respond within the deadline shown on your summons. Our partner Solo helps you file an Answer to prevent default judgment.

If the debt appears on your credit report, dispute it with the credit bureaus. Collectors still need to validate the debt.