What Is a Debt Settlement Agreement and How Does It Work?

A debt settlement agreement is a legally binding document that resolves disputes without going to trial. You can often settle debt collection lawsuits for 30-60% of what you owe if you negotiate effectively and get all terms in writing.

Settle Your LawsuitA settlement agreement can help you bypass lengthy and costly litigation. You can offer to settle instead of enduring a debt collection lawsuit. The court will dismiss the case if the debt collector accepts your offer.

The settlement agreement is a legally binding document. Both parties must fulfill its terms. Before agreeing to or offering a settlement agreement, you must understand how these documents work. You also need to ensure the settlement offer serves your best interests.

Negotiate Your Debt Settlement Before the Court Deadline

Debt collectors often accept 30-60% of what you owe to avoid court. Our partner Solo helps you negotiate and settle your lawsuit fast, all online.

Settle Your Debt NowUnderstanding settlement agreements can save you time, money, and stress. Here’s what you need to know.

What Is a Settlement Agreement?

You can resolve disputes in or out of court. Settlement agreements offer a path to resolution without trial. The decision depends on the type of dispute and each party’s willingness to compromise.

A settlement agreement states the terms under which the court may dismiss an ongoing lawsuit. The document outlines the resolution to a dispute. Opposing parties negotiate, compromise, and sometimes change terms before reaching an agreement.

The party making the offer should sign in acceptance of the conditions. Your opponent should also sign and date to show agreement. Both signatures make the document legally binding.

Settlement agreements work in almost all areas of life. These agreements can help resolve issues from:

- Property allocation in divorce

- Employment disputes

- Personal injury claims

- Defective products

- Medical malpractice

- Debt collection lawsuits

Many debt collectors are willing to settle for less than the original amount owed. Our partner Solo helps consumers negotiate and settle debt collection lawsuits effectively.

Essential Elements of a Settlement Agreement

A well-drafted settlement agreement should contain all necessary details. If you are drafting the document, include the following:

- Full names of both parties

- Detailed recitals (incidents that caused the conflicts)

- Terms of release

- Consideration (specific payable amounts or conditions both parties must implement)

- If a lawsuit is already in court, include the case name

Remember that a settlement agreement does not address liabilities. Its sole purpose is to bring the dispute to an end.

The court only enforces the agreement as written. It is not the judge’s duty to set settlement conditions for you. You should research and determine the facts of the case. You need to understand the best outcome a settlement agreement can provide.

What to Include in Your Settlement Agreement

Settlement agreements work for all kinds of disputes. What you include depends on the issue you hope to settle. In general, every settlement agreement should ask for the following.

Determine the Terms

When drafting a settlement agreement, you should ask the opposing party to agree to specific terms. For instance, a debt collector can accept to withdraw a lawsuit.

Example: XYZ debt collectors sued Dan for an outstanding debt. He knew the debt was his and the amount was correct. But he also knew he couldn’t afford the total amount. After filing his Answer with the court, he proposed a debt settlement. Dan asked that XYZ Collection accept a lump-sum payment of a percentage of his debt. He also asked them to withdraw the lawsuit and mark the account as paid. The company agreed and drafted the debt settlement agreement with these conditions. Dan avoided collection calls and a stressful case.

The Consideration

The consideration is the offer that ends the dispute. In a debt collection lawsuit, it is the amount of money you are offering. In a different type of dispute, it may not involve money.

Suppose you are injured in a car accident and prefer to resolve the issue without a lawsuit. In the personal injury settlement agreement, you can ask the driver to pay your medical bills. You can also request compensation for loss of income during recovery.

You have the power to negotiate a settlement that works for your financial situation. Our partner Solo has a proven history of helping consumers settle debt collection lawsuits for much less than they owe.

Set a Deadline for Implementation

You should state any deadlines for both parties taking or stopping specific actions. For example, if you propose a debt settlement amount, mention the date you must make the payment.

Clear deadlines prevent confusion and ensure both parties fulfill their obligations.

Set the Date of Effectiveness

The settlement agreement typically releases one or both parties from possible future action. You should mention the date when the contract goes into effect.

Is it on the day both parties sign? Or is it when the court dismisses the case? Both parties should clearly understand and agree with the set dates.

Ask the Other Party to Sign the Agreement

Remember to sign and date the settlement agreement. You should also allow space for your opponent to sign and date. Any mediators or witnesses present can also sign, although this is usually unnecessary.

Both signatures make the agreement legally enforceable.

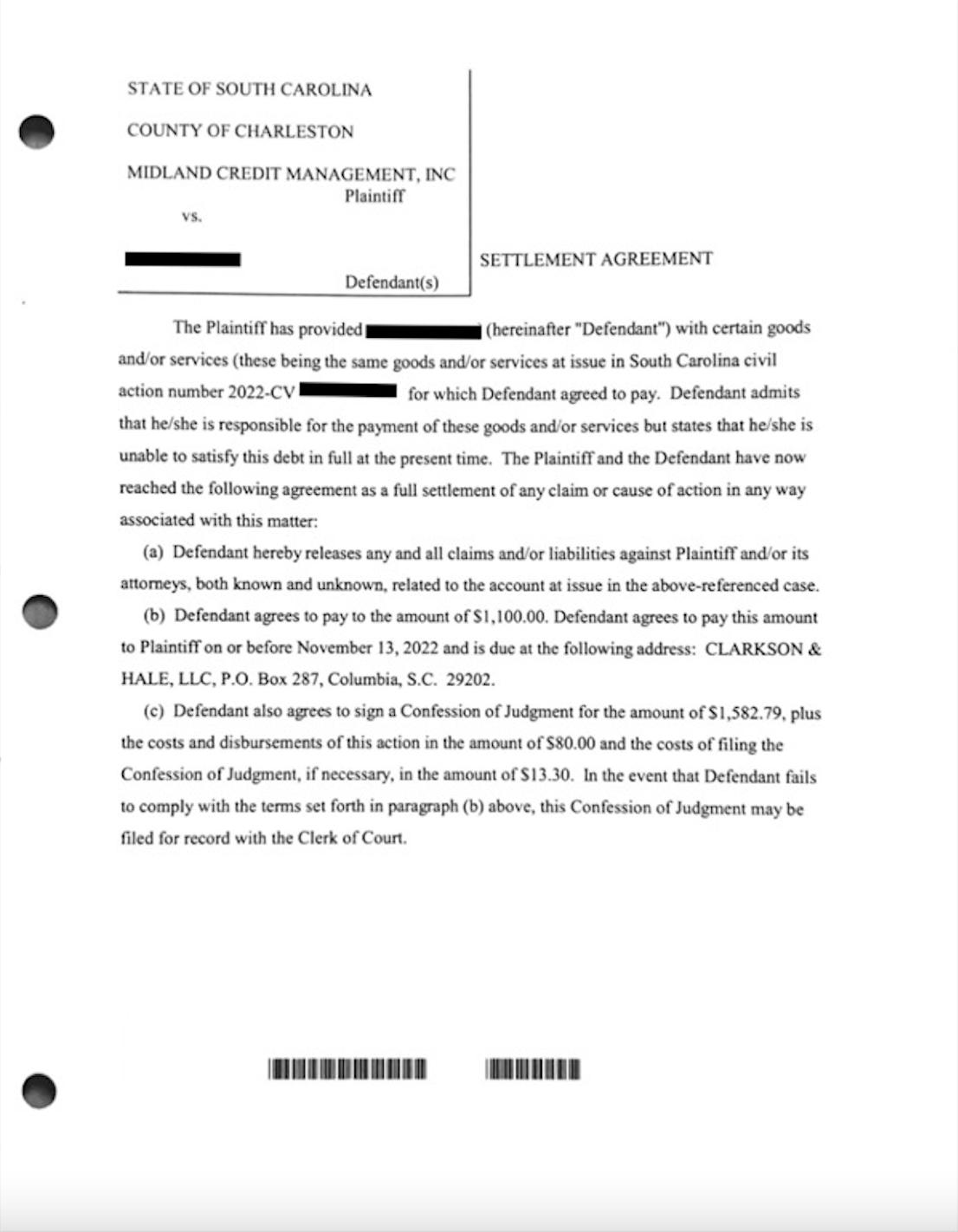

Debt Settlement Agreement Example

A debt settlement agreement is a legal document filed into a debt collection lawsuit. It shows that both parties have reached a consensus on how to resolve the dispute.

Below is an example of a debt settlement agreement in a South Carolina debt lawsuit:

The example shows how clear terms and specific dates create a binding agreement. You can use this as a template for your own negotiations.

Why You Should Consider a Debt Settlement Agreement

Debt settlement agreements can be a lifesaver if you are facing a debt collection lawsuit. They take away the stress, time, and money that come with court cases.

Many debt collectors are willing to settle a debt for less than the original amount owed. Settling saves them time and resources as well.

However, before signing a settlement agreement, you need to be sure you understand the terms. You should also state your demands and clearly explain the reason for the dispute.

Keep in mind that once the court dismisses the case, it is not under obligation to mediate between you and your opponent. The judge can only enforce the terms of the contract. Only sign when you are satisfied.

You may need to speak with an attorney to get the legal advice you need. You can also check out our article on How to Make a Debt Settlement Agreement.

How to Negotiate a Better Settlement

Negotiating a settlement agreement requires strategy and knowledge. You need to understand your rights and the collector’s limitations.

Start by reviewing the debt details. Confirm the amount owed and verify the debt collector has the legal right to collect. Check the statute of limitations on your debt.

Determine what you can realistically afford to pay. Debt collectors often accept 30-60% of the original debt. Make an initial offer lower than what you can actually pay. This gives you room to negotiate.

Get everything in writing before you make any payment. Never agree to terms over the phone without written confirmation. The settlement agreement should clearly state the collector will mark the account as paid and dismiss any lawsuit.

You deserve a fair settlement that doesn’t leave you financially devastated. Professional help can make the negotiation process smoother and more successful.

What Happens After You Sign

After both parties sign the settlement agreement, you must fulfill your obligations. Pay the agreed amount by the deadline specified in the agreement.

Keep copies of all documents related to the settlement. Save your payment confirmation and the signed agreement. These documents protect you if disputes arise later.

The debt collector should dismiss the lawsuit once you fulfill the terms. They should also report the account as settled or paid to credit bureaus. Verify that the collector has updated your credit report correctly.

If the collector fails to honor the agreement, you have legal recourse. The signed settlement agreement is enforceable in court. You can file a motion to enforce the agreement.

Monitor your credit report in the months following the settlement. Ensure the debt is properly reported and no collection activity continues.