Make Stephen Einstein Validate Your Debt in 5 Simple Steps

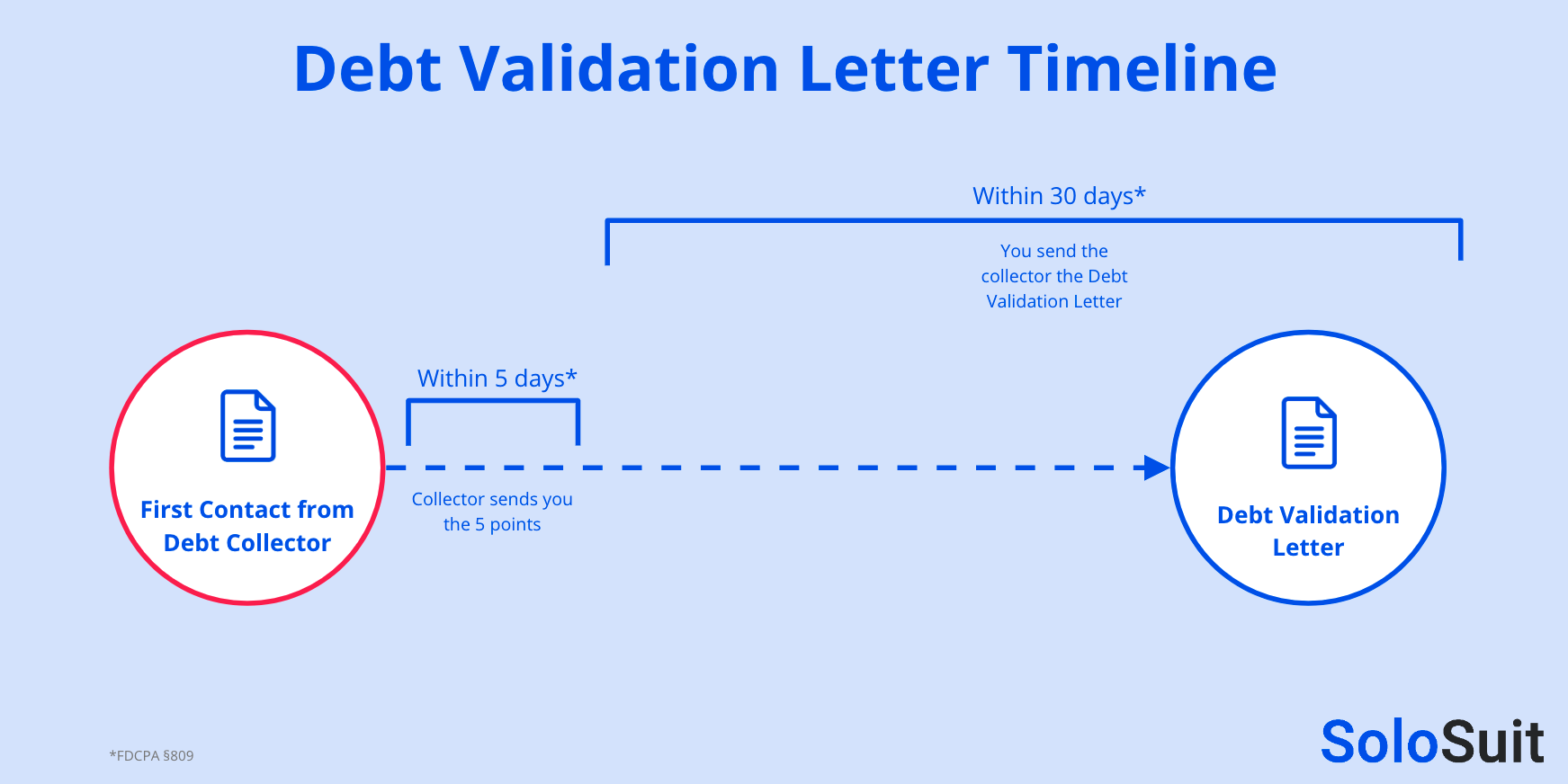

If Stephen Einstein contacts you about a debt, you have the legal right to demand validation before paying. Send a debt validation letter within 30 days to force them to prove the debt is yours and the amount is accurate. If they sue you, respond with an Answer within your state's deadline to protect your rights.

Answer Stephen EinsteinHas Stephen Einstein contacted you about an unpaid debt? Are you confused about what you owe and why?

Debt collectors often skip proper documentation to create panic. They want you to pay without questioning anything.

Stop Stephen Einstein's Collection Calls Now

Send a professional debt validation letter today and pause all collection activities. You have only 30 days from first contact to exercise your FDCPA rights.

Create Your ResponseYou have rights. The Fair Debt Collection Practices Act (FDCPA) gives you the power to demand debt validation.

A validation request forces collectors to prove the debt is real. They must confirm you actually owe it and the amount is correct.

Understanding Stephen Einstein’s Collection Tactics

Stephen Einstein is a debt collection law firm. They work for businesses trying to recover money from consumers.

Their goal is simple: get you to pay by any means necessary. Sometimes they cross legal lines.

Most Stephen Einstein employees are non-attorney collectors paid on commission. More money collected means bigger paychecks for them.

Consumers have sued Stephen Einstein multiple times for FDCPA violations. The FDCPA protects you from:

- Misleading or false information

- Deceptive collection tactics

- Harassment and abusive behavior

- Falsified debt claims

When Stephen Einstein first contacts you, they must provide debt details. If they don’t, you can force their hand with a debt validation letter.

Why Debt Validation Protects You

Requesting validation serves four critical purposes:

1. Confirm the Debt Belongs to You

Name mix-ups happen. Record-keeping errors occur. Identity theft is real.

Validation proves whether you actually owe the debt or not.

2. Verify the Amount Is Accurate

Maybe you already made payments. Perhaps they inflated the numbers.

Validation shows exactly how they calculated your balance.

3. Identify Who Actually Owns the Debt

Original creditors often sell debts to third parties. You need proof the collector legally owns your debt.

4. Confirm Legal Authorization

Your creditor must legally authorize Stephen Einstein to collect from you. Validation confirms this authorization exists.

Skipping validation could mean paying someone else’s debt. It could mean paying inflated amounts or dealing with unauthorized collectors.

Our partner Solo can help you draft a professional debt validation letter quickly.

What a Debt Validation Letter Does

A debt validation letter demands proof you owe the specified debt. The FDCPA gives you this right without penalty.

Once Stephen Einstein receives your letter, they must pause collection activities. They cannot contact you until they provide proper validation.

Sometimes collectors stop pursuing the debt entirely rather than validate it. Why? They lack sufficient proof.

Proper debt verification must include:

- The exact amount owed

- The original creditor’s name and address

- A 30-day dispute notice

- A statement about obtaining verification if you dispute within 30 days

Your validation letter should use proper legal language. You want Stephen Einstein to know you understand your rights.

When to Skip Debt Validation

Sometimes requesting validation backfires. Here are three situations where you should avoid it:

You’re Ready to Settle

You know you owe the debt. You have money to pay it.

Extra paperwork may frustrate collectors and reduce negotiation flexibility. They might even file a lawsuit out of annoyance.

Your Statute of Limitations Is Almost Up

If your debt expires soon under your state’s statute of limitations, stay quiet. Sending a validation letter alerts collectors to the deadline.

Worse, acknowledging the debt may restart or extend the statute of limitations in some states.

Your Original Creditor Is Well-Organized

Major credit card companies keep meticulous records. They won’t lose your documentation.

Validation requests against organized creditors often trigger more aggressive collection efforts.

Your 5-Step Debt Validation Process

Follow these steps after Stephen Einstein contacts you:

- Send a professional debt validation letter within 30 days of initial contact. Wait for their response.

- If they don’t respond, resend the letter with your receipt. Include a statement that you won’t pay unvalidated debts per FDCPA law.

- If Stephen Einstein reported to credit bureaus without validating, demand they remove the notice.

- If they send accurate validation, they can resume collection activities legally.

- Consult an attorney if you need help negotiating payment plans or removing items from your credit report.

Debt validation protects you from unfair practices. It prevents costly mistakes in the collection process.

Our partner Solo makes creating validation letters simple and fast.

What Happens If Stephen Einstein Sues You

If Stephen Einstein files a lawsuit, you must respond with an Answer. Filing an Answer protects your rights and prevents wage garnishment.

Most states give you only 14-30 days to file. Missing this deadline means automatic judgment against you.

An Answer disputes their claims and presents your defenses. You can raise issues like:

- Statute of limitations expiration

- Lack of proper documentation

- Incorrect debt amounts

- Identity verification problems

Courts take your Answer seriously. Many debt collectors drop cases when you respond properly.

Take Control of Your Debt Situation Today

Stephen Einstein relies on consumer confusion and fear. They hope you’ll pay without asking questions.

You now know better. You understand your validation rights under federal law.

Send that validation letter. Make them prove their case. Protect yourself from paying debts you don’t owe.

Act quickly if you’ve received a summons. Time limits are real and unforgiving.

You have more power than debt collectors want you to believe. Use it.